A balancing act: How Singapore’s policies reduce risk and control inflation

A balancing act: How Singapore’s policies reduce risk and control inflation

By SMU City Perspectives team

Published 24 July, 2023

Organisations and individuals must monitor trends in external developments, be agile in learning to adapt to disruptive changes and collaborate with others to better cope in our complex world.

Chow Hwee Kwan

Professor of Economics and Statistics (Practice), Singapore Management University

In brief

- Singapore uses an exchange-rate-based monetary-policy framework, which centres on managing the Singapore-dollar exchange rate instead of the benchmarked interest rate. This is more suitable as import prices dominate Singapore’s economy.

- This framework has been effective and provided a low-inflation environment that is conducive to sustainable growth, helping the economy weather external economic shocks over the past decades.

- Managing this exchange rate has become more challenging with the increasingly connected nature of world economies. However, past data suggest the value of the Singapore dollar had been largely reflecting the country’s longer-term economic conditions.

It sounds like a truism, but the economy works best when there is price stability — when inflation is low, stable and predictable. This is because people and businesses are better able to plan how they save, spend and invest, which are needed to help the economy to grow.

Even when global markets are increasingly volatile and economies fluctuate, Singapore’s monetary-policy framework continues to remain effective in maintaining price stability here.

In her paper, “Achieving price stability”, Chow Hwee Kwan, Professor of Economics and Statistics (Practice), delves into Singapore’s monetary policy and investigates if there is a need for the framework to change as the nation develops into a more mature economy.

Starting by explaining the basis of Singapore’s monetary-policy framework and how it works to achieve price stability, her study goes on to examine the importance of different macro- and microeconomic policies that help to maintain confidence in our economy.

A unique exchange-rate-based policy framework

The stated objective of the Monetary Authority of Singapore (MAS) is to deliver medium-term price stability in order to facilitate sustainable growth in the Singapore economy. To achieve this, MAS has adopted an exchange-rate-based monetary-policy framework since 1981, which is centred on managing the Singapore-dollar exchange rate, instead of the benchmarked interest rate used in other countries.

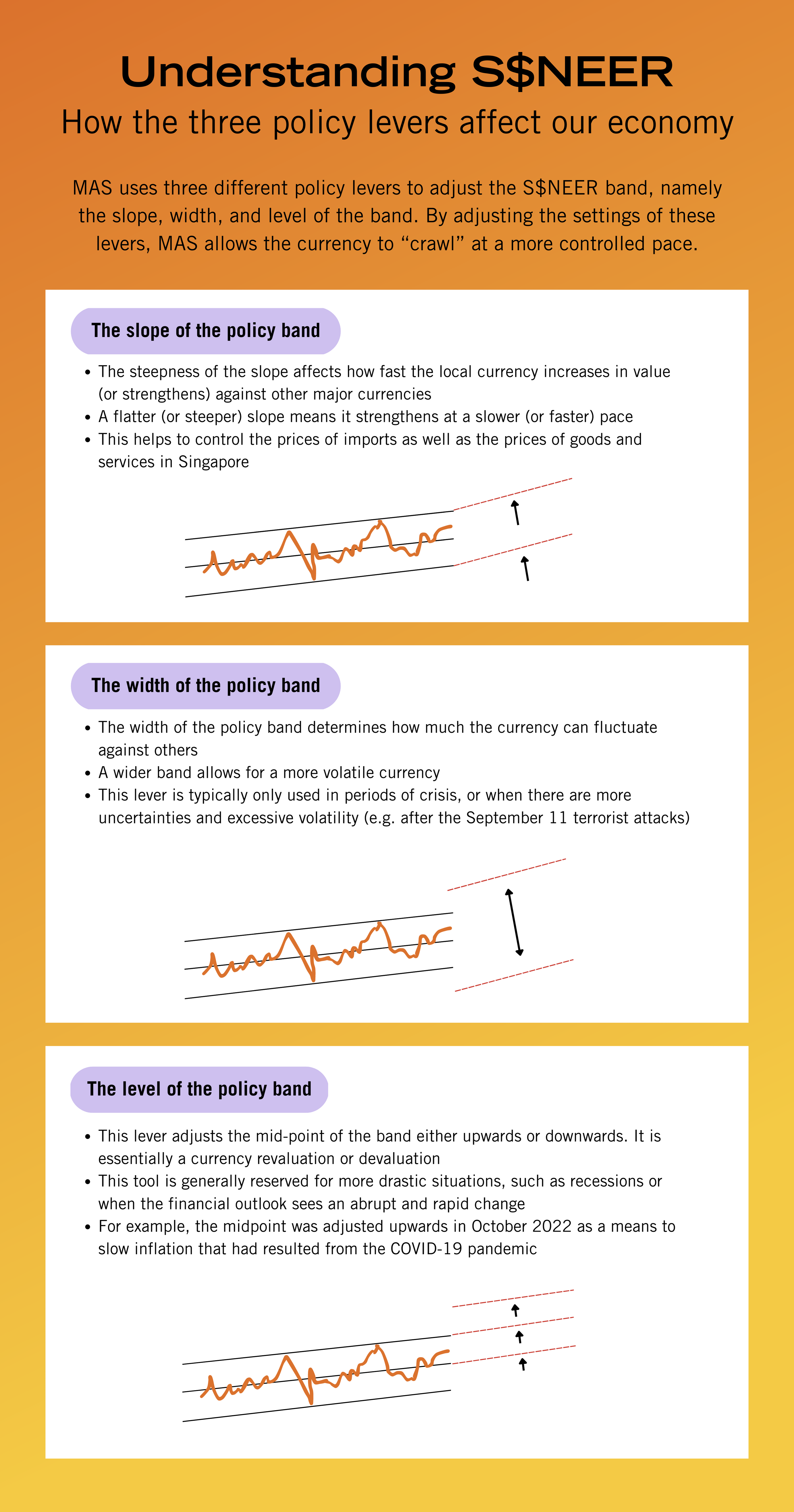

Under this system, MAS lets the local dollar rise or fall against the currencies of Singapore’s main trading partners within an undisclosed band, also known as the Singapore dollar nominal effective exchange rate (S$NEER). The band is set by MAS, the central bank, to “bring core inflation closer to its historical average of just under two per cent in the medium term”.

This exchange-rate-based framework has been shown to be more suitable for Singapore, as import prices dominate the economy. Using the interest rate as the key monetary-policy instrument in Singapore is not appropriate as there is little to no control on how money flows between foreign and local currency.

MAS uses three different policy levers to adjust the S$NEER band, namely the slope, width, and level of the band (see infographic). An assessment is made of the balance of risks to Singapore’s growth and inflation every April and October, after which MAS decides whether to change one or more of these levers – or make no changes at all. Changes can also be made outside of this regular cycle in periods of crisis, such as during the ongoing COVID-19 recovery period.

The central bank says S$NEER adjustments are a more effective tool to handle Singapore’s small and open economy, which has high volumes of trade and cash flow. Plus, domestic inflation is influenced by import prices due to Singapore’s high percentage of imports, and that the country is a price-taker in global markets.

This framework has served Singapore’s economy well over the past decades, providing a low-inflation environment that has been good for sustainable growth. Up till 2021, the year-on-year headline inflation was low, at an average of 1.6 per cent, and stable. This tends to be lower than in other Asian countries like South Korea, Malaysia, Taiwan, and Thailand.

Response to the effects of COVID-19

“In April 2020, early on in the COVID-19 pandemic, both the slope and level of the policy band were adjusted simultaneously to ease monetary policy,” Prof Chow says.

“The policy band was flattened and the band’s centre was lowered to the prevailing S$NEER level. This provided the advantage of catering to an abrupt shift in economic activity, while allowing for a gradual change in economic activity over the medium term,” she explains. This was part of what MAS describes as an accommodative policy stance, which sets the policy band on a zero per cent appreciation path to accommodate the downshift in inflation.

In the two monetary policy reviews that followed, in October 2020 and April 2021, this same accommodative monetary-policy stance was maintained. Since then, however, MAS has repeatedly tightened monetary policy, in response to the inflation surge that was observed as the pandemic dragged on. This was first pre-emptively done in October 2021, then a surprising move as reported by Reuters, where most other central banks at that time chose to maintain a looser monetary-policy stance.

This has since been followed by four additional instances of tightening Singapore’s monetary policy, including two adjustments outside of MAS’ October/April evaluation cycle. These off-cycle adjustments are made when the central bank sees a need to adjust the policy due to ongoing economic activity.

Click the dates to learn more

A study on the effectiveness of Singapore’s monetary policy framework

In order to understand how effective Singapore’s exchange-rate-based monetary policy framework is, Prof Chow studied if the Singapore dollar suffered from any severe or persistent currency misalignment and if so, how it did. Avoiding currency misalignment is a balancing act since an undervalued Singapore dollar means our imports of goods and services are more expensive, which could raise business costs and the cost of living for citizens. Conversely, an overvalued Singapore dollar means a country’s exports of goods and services are relatively more expensive, which could lower our business’ international competitiveness and possibly higher unemployment.

Her analysis looked at the difference between the Singapore dollar’s observed real effective exchange rate (REER) and its “estimated equilibrium” level. To compute the estimated equilibrium level, she considered various factors that could lead to a serious misalignment. One example is Singapore’s terms of trade, the ratio of our export prices to import prices, which has risen over the years as our economy moved up the value chain and exported higher-value products. Hence, the Singapore dollar was managed to appreciate over the long term to avoid an undervaluation of the currency.

From the 1990s, the actual REER appeared to parallel its “estimated equilibrium” value rather closely, which suggests that there is no serious misalignment. This data confirms the value of the Singapore dollar is largely aligned with our economic fundamentals suggesting large abrupt adjustments down the road is unlikely.

Given this result, Prof Chow states in her paper that the exchange-rate-based monetary policy framework remains effective and there is no urgent need for reformulation of the overall policy.

Mitigating risks amid increasing volatility

Moving forwards, managing this nominal exchange rate has become more challenging, with exchange-rate fluctuations impacted by the increasingly connected nature of world economies. This means that global and regional developments will result in stronger effects on Singapore’s economic activity. For instance, quantitative easing by the central banks in the advanced countries had led to greater flows of money into Singapore and made our exchange rate more volatile.

To handle these effects, monetary policy in Singapore has to be supported by macroprudential policies that can mitigate risks to the country’s financial stability. Many of these are primarily targeted at cooling Singapore’s property market, given the adverse implications the market could have on individual households, the banking system and the broader economy. “Such policies include lowering the loan-to-value and total debt-servicing ratios and raising additional buyers’ and seller’s stamp duties,” Prof Chow explains, referencing the housing-market measures that have been announced since December 2021.

Exchange-rate management works better in an environment where there is a high level of confidence in the economy, making it especially important for Singapore to maintain this confidence. This makes it even more essential to have a consistent framework of macroprudential and other economics policies in order to ensure that the exchange-rate-based framework continues to function smoothly.

Offering advice to Singapore’s businesses and citizens who are concerned about the economic challenges that lie ahead, Prof Chow says, “Organisations and individuals must monitor trends in external developments, be agile in learning to adapt to disruptive changes and collaborate with others to better cope in our complex world.”

Methodology & References

- Chow H.K, Xie T.(2021). Achieving price stability. Singapore Management University. Retrieved from: https://ink.library.smu.edu.sg/soe_research/2496/

- Monetary Authority of Singapore. Monetary Policy Framework. Retrieved from: https://www.mas.gov.sg/monetary-policy/Singapores-Monetary-Policy-Framework

- Tang, S.K (2019). The S$NEER and its slope, width and centre: Questions about Singapore’s monetary policy. Channel News Asia. Retrieved from: {https://www.channelnewsasia.com/business/sneer-and-its-slope-width-and-centre-questions-about-singapores-monetary-policy-856746}

- Aravindan A., Daga A. (2021). Singapore tightens monetary policy in surprise move as price pressures grow. Reuters. Retrieved from: https://www.reuters.com/world/asia-pacific/singapore-central-bank-tightens-policy-surprise-move-2021-10-14/

- SRX. Singapore's New Property Market Cooling Measures, Latest Updates 2023. Retrieved from: https://www.srx.com.sg/cooling-measures